Intalytics Commentary: The Real Estate “Do-Over”

When I was a child (more years ago than I care to remember), the concept of the “do-over” was sacrosanct when playing sports. Most of our games were played without the benefit of adult supervision, and we were forced to reconcile any differences of opinion concerning a certain play among ourselves. (“I was safe! You were not – you were out!”) When we couldn’t agree on the outcome, we resorted to a “do-over” – ignoring the at-bat or football snap that had just taken place and doing the play over again.

Most retailers, restaurants, and other tenants (banks, healthcare providers, etc.) in the U.S. have a unique opportunity to conduct a “do-over” with their real estate portfolios. As a rule, retailers have done an effective job of synchronizing their store deployments with localized supply and demand – opening new stores when the opportunity presents itself, and closing stores that are no longer generating a profit or acceptable financial return. Over the past 10 years (following the Great Recession of the late 2000s), most retailers made store deployment changes on an incremental basis, slowly opening and closing stores as appropriate.

Our current pandemic-induced recession* will force most retailers to make immediate and far-reaching changes to their portfolio. There are several factors contributing to these changes:

- Social Distancing – instituted in a widespread fashion in the U.S. to slow the spread of the coronavirus in March 2019, this phenomenon will likely continue to some extent until after a vaccine is developed and made readily available. While this will likely have a short-term impact on shopping and entertainment behavior, even that impact will be very harmful to selected operators – ex. bars, sit-down restaurants, trampoline parks, gyms/fitness centers, and other environments that include close contact with others.

- Operating Expenses – consumer demands for changes in store and restaurant operating environments will have the unenviable impact of simultaneously reducing sales (maintaining 6-foot minimum distance between restaurant patrons results in lower revenue during peak times) and increasing operating costs (retrofitting stores with plexiglass shields, providing personal protective equipment). As such, even assuming no shopper reluctance to shop or dine out, store sales and profitability will be eroded.

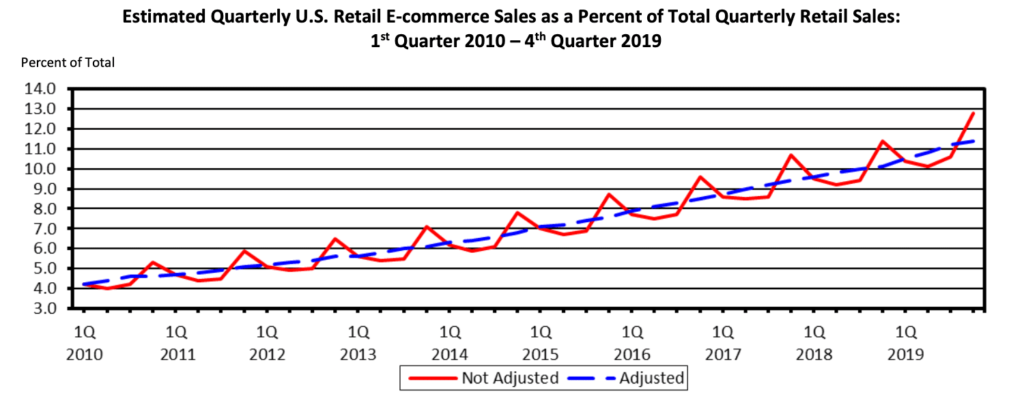

- E-Commerce – the proportion of total retail sales accounted for by e-commerce grew at a steady pace through CY 2019, as the following graph illustrates:

E-commerce’s proportion of total retail sales has skyrocketed during the pandemic, due to a combination of state-ordered store closures and an increased unwillingness of consumers to shop in open brick and mortar stores. This sudden acceleration of the proportion of total retail sales represented by e-commerce may see retailers catapulted into a brick and mortar vs. e-commerce environment that otherwise may not have been reached until 2023 or 2024. Experiencing an annual average ~1% erosion of brick and mortar retail sales requires a regular fine-tuning of a store portfolio – a massive acceleration of that erosion is a shock wave.

- Recession – on top of all of these factors, the U.S. is entering into a recession which will have a significant impact on consumer expenditures regardless of the economic stimulus and bailout packages enacted by the federal government. While certain operators such as dollar stores, value retailers, and quick service restaurants may benefit from a recession, most – including sit-down restaurants, apparel stores, and department stores – will be severely impacted.

The impact of these factors will force a significant shift in the store portfolio for most tenants in the U.S. A majority of operators will need to downsize (and in certain instances, significantly reduce their brick and mortar footprint), while certain operators will be able to maintain or even expand their current footprint – think grocers and food delivery operators. How can retailers determine what store deployment will help to ensure a profitable future?

There are several key variables that each operator will need to consider when determining their optimal store portfolio going forward:

- Recession Sensitivity – how attractive will your concept be during a recession? The apparel industry has been significantly impacted by e-commerce, and mid- to high-end apparel stores will likely be further impacted by an economic downturn. On the other hand, value operators such as TJ Maxx and Burlington Stores will likely gain market share, given their compelling value proposition.

- E-Commerce Mix – how effectively can your operations provide a true omni-channel shopping experience for consumers? Some operators were well on their way to effectively combining in-store and online shopping before the pandemic – consider Williams-Sonoma, which generated over 50% of their sales from e-commerce in FY 2018. Others are only just beginning to develop a true omnichannel offering, which will inhibit their ability to retain market share, or have no meaningful on-line presence.

- Competition – how will the COVID-19 Recession impact competition? In particular, how many competitors will close stores or go out of business, freeing up market share for remaining operators to capture?

- Real Estate Availability – in a perverse way, the impending number of store closures will result in real estate availability for those operators planning to expand. Hard-to-get real estate (or “lifetime” deals) will no longer be a major concern – any market or neighborhood that a retailer wants to expand into will likely have availability.

How can retailers determine the most appropriate store deployment scenario for the future? Intalytics has been conducting sensitivity analysis for operators, typically generating 3 alternate optimal store deployment scenarios (Best Case, Expected Case, and Worst Case). Intalytics works closely with each operator to review the impact that the aforementioned factors are likely to have on store performance, and then generates an optimal brick and mortar strategy that maximizes the number of profitable stores that can be supported. As part of this exercise, Intalytics identifies the following specific recommendations:

- Existing Store – Retain

- Existing Store – Relocate

- Existing Store – Consolidate (2-for-1)

- Existing Store – Close

- New Store – Open

The resulting recommendations include annual sales projections for each location, including the sales recapture impact of store closures, the store transfer/cannibalization impact of new store openings, and the impact that store openings or closures have on e-commerce sales. Furthermore, new store recommendations include the specific recommended location (such as shopping center or urban street location). The entire analysis is conducted from a bottom-up, granular level, to ensure that it accurately accounts for localized consumer shopping behaviors.

Leveraging the results of the Best Case / Expected Case / Worst Case brick and mortar scenarios, management teams are positioned to make more informed decisions concerning real estate disposition and acquisition over the next 1-2 years. Some operators may take a more risk-averse approach – assume a Worst Case scenario, and then be prepared to pivot if comp store sales growth is more akin to an Expected Case or Best Case scenario. Others may follow the Expected Case path, while still others may follow the Best Case scenario in an effort to gain market share and emerge as a dominant player. In any case, the management team is in a position to make strategic decisions concerning their overall real estate deployment and capital investment, while tactically knowing which specific locations to pursue.

For more information on how Intalytics can support your organization’s efforts to inform brick and mortar strategy, please contact us to schedule an initial discussion.

* While we are not technically in a recession as yet given the requirement of two consecutive quarters of significant decline in economic activity, there is no doubt that will soon officially be the case.

Related News

Carousel items